Progressive should unite to help Simon Hughes make the Budget fairer. Progressive taxation and a slower reduction plan are the way ahead.

The Government’s claims that the Budget was “tough but fair” and “progressive” have quickly unravelled following analysis by the Institute for Fiscal Studies, Financial Times, and by Tim Horton and Howard Reed on this blog. Despite Nick Clegg’s nonsensical protestations that the the IFS analysis did not include as yet undefined “future changes”, Lib Dem deputy leader Simon Hughes has conceded the point and is now urging Lib Dems to “come forward with amendments … [to the Budget that] improve fairness and make for a fairer Britain”.

Progressives of all stripes should help Mr Hughes with his mission. Lib Dem policies like a Mansion Tax and Capital Gains Tax would relieve pressure for the regressive policies in the Budget. But we should also work to challenge another Coalition myth which continues to have traction.

{kind=link}

While the post-Budget analysis has focused on distributional elements, the broad left has been unable to win the argument that the scale and speed of Osborne’s Budget was a matter of choice. Instead the public and media appear to have accepted the Tory line that the total package of cuts worth £128 billion by 2015-16 was “unavoidable” because of “Labour’s debt crisis“.

This reflects considerable political skill by George Osborne and David Cameron in talking relentlessly about the risk of a Greek-style “sovereign debt crisis” and encouraging their Lib Dem colleagues to use the same language. But blame also lies with the Labour party, which refused to hold a comprehensive spending review before the election.

In the March Budget, Labour set out plans to “halve the deficit over four years.” They announced costed plans to increase taxes by £18 billion by 2013-14 and set out a desire to cut spending by £39 billion over the same period. But they failed to detail where the money would come from allowing George Osborne to say in his Budget speech, “What we have not inherited from our predecessor is a credible plan to reduce their record deficit.” Osborne is right and yet this does not necessitate the additional £32 billion in pain by 2013-14, rising to £40 billion by 2104-15, and up to £55 billion in 2015-16.

As outlined on Left Foot Forward on Tuesday, the decision to raise VAT was only necessary to pay for tax cuts for businesses including banks, the Lib Dems’ regressive tax threshold pet project, and to meet Tory promises on national insurance. The additional cuts have been made out of an ideological desire to erode the “structural deficit” in its entirety by 2015-16 putting growth and employment at tremendous risk. Three points are worth making.

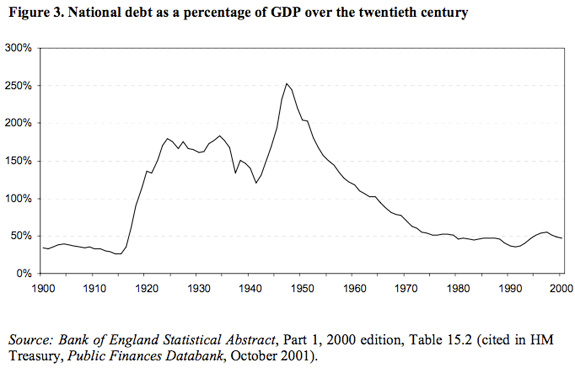

First, until the financial crash Labour had succeeded in keeping national debt below the 40 per cent of GDP target that it set itself. In 2006/07, public sector net debt was 36.0 per cent of GDP. It rose rapidly primarily because of “financial interventions” to help the banking sector and because of the unemployment benefits and lost tax receipts caused by the recession. It currently stands at 62.2 per cent and under Labour plans was projected to peak at 74.9 per cent in 2014-15. As this graphic using data from the OECD shows, even at that level, the UK will be below a number of countries including Italy, Japan, and indeed Greece. Under the Tory plans net debt will now peak only marginally below Labour’s 70.3 per cent in 2013-14 – although if the Budget causes the economy to slow down by more than predicted

{kind=link}

{kind=link}

Second, the “structural deficit” was caused primarily by the recession not by Labour’s pre-crash spending plans. Left Foot Forward has been fond of showing this graph. Although Gordon Brown should have closed the gap earlier, it shows how in 2008, current spending and tax receipts were virtually in balance. The deficit was due to the Government’s capital spending programme which was perfectly sustainable while the economy grew. Crucially, it was only in November 2008 – in the midst of the banking crisis – that the Tories dropped their pledge to match Labour’s spending plans. At the time, Nick Clegg said, “David Cameron has learned nothing. It’s exactly what the Conservatives did in the 1980s.”

{kind=link}

Third, markets were satisfied with Labour’s approach. There was much guff during the election campaign about what impact a hung parliament would have on markets. Similarly there was never any evidence that a Labour victory would result in Britain losing its AAA credit rating. Not least because markets knew the truth about debt levels and the deficit. Indeed, the yield on British Government Securities have been at historically low levels since the financial chaos of autumn 2008. Yields remained around 4 per cent through both the November 2009 pre-Budget report and the March 2010 Budget when Labour set out their deficit reduction plans.

{kind=link}

During his Budget statement, George Osborne admitted that, “this was a crisis that started in the banking sector.” Indeed it was. But because of Cameron, Osborne – and now Clegg, Alexander and Cable’s – ideological position to cut deeply and rapidly, the next crisis may be caused by the government. The alternative is a fairer and slower deficit reduction plan.

Left Foot Forward doesn't have the backing of big business or billionaires. We rely on the kind and generous support of ordinary people like you.

You can support hard-hitting journalism that holds the right to account, provides a forum for debate among progressives, and covers the stories the rest of the media ignore. Donate today.

20 Responses to “Progressives should unite for a fairer, slower reduction plan”

Fat Bloke on Tour

Will

You need to work on your analysis if you are going to say that AD had not put in place a credible deficit reduction plan. He had and the figures were there to show it.

Part One: The Curious case of the shrinking Output Gap

The whole argument revolves around the structural / cyclical deficit question and how this has been manipulated by the Treasury to show the story it wants to sell.

2009/10

Total Deficit = 11.1%

The OBR using Treasury figures and methodology along with some changes to Trend growth generated the following split:

1) Structural Deficit = 8.8% of GDP up from the Treasury’s earlier view.

From memory that was figure was in the region of 8.0%.

2) Cyclical Deficit = 2.3%

Now the structural deficit is a derived number, the cyclical deficit is calculated and then taken away from the actual deficit. This then leads to the output gap as this is the number used to generate the cyclical deficit. The output gap is the difference between an economy’s potential output and what it actually produces.

Output gap and Cyclical deficit are linked as follows —

Cyclical Deficit = Output gap (Year Y) x 0.5 + Output gap (Year Y-1) x 0.2

Consequently the output gap has a huge and direct bearing on the structural deficit.

Now the fun starts:

2009/10 Treasury Output Gap = 6%

2009/10 OBR Output Gap = 4%

Therefore the cyclical deficit magically reduces from 3.1% of GDP to 2.3% of GDP all at the stroke of an OBR pen and the fact that they have reduced the trend rate of growth over past two years.

All this in light of a 6.2% reduction in GDP and two years’ish of trend growth lost in the process.

Consequently you could say that the Credit Crunch lost the country 10/11% of GDP.

The question is how realistic is the output gap figure of 4%.

The better question would be how realistic would an output gap figure of 6% be?

Both figures do not to me seem to capture the dormant capacity of the country at the moment.

Yet the lower figure is being used to maximise the structural deficit figure which is then being used to scare the troops into accepting the Coalition / Establishment’s Dog Boiling agenda to neuter the TB / GB settlement regarding the scope and quality of the public sector.

The OBR suggests that after 5 years of bobbling along at or below trend we reached Dec 2007 with GDP less than 1% above trend, nothing controversial there but to suggest that after the hell of the Credit Crunch and the 8% ILO unemployment rate and all the people flexing their time to keep their jobs to suggest that we now have economic activity 4% below trend suggests that the “Three Brothers Grimm” of the OBR do not live or interact with the real world.

And it gets worse.

What is the OBR story for 2010?

2.1% trend growth and 1.3% actual growth predicted.

What happens to the output gap?

Slight enlargement due to the slow growth?

No you would be wrong, the OBR see the output gap closing over the next 12 months.

Really the Emperor’s three little helpers are dancing bollock naked through Liverpool Street station as I speak.

DrKMJ

Progressives should unite for a fairer, slower reduction plan http://bit.ly/bXgL4t via @leftfootfwd

Fat Bloke on Tour

Will

Part Two: Bend it like Beckham or Deficit Forecasting and the Treasury

Starting off with some numbers for 2009/10

As always these are from memory and contain the odd schoolboy howler.

Budget – March 2009 = £175bill forecast.

PBR – Nov 2009 = £178bill forecast.

Not looking good for AD’s pre-election boom-let sorry targeted investment package.

Budget March 2010 = £165bill estimate.

May 2010 = £156bill.

That is the non financial intervention view of the budget deficit for 2009/10.

In cash terms things were even better as we seemed to generate cash from our bank holdings.

£156bill = 11.1% of GDP

£50bill = Investment / 3.5% of GDP, something to be proud of.

£106bill = Current Deficit.

Investment can be broken down into gross and net with net investment being in the region of £35bill’ish / 2.3 or 2.5% of GDP.

Other way of looking at it breaking down the headline number into structural and cyclical.

The £156bill headline number then becomes:

£33bill = Cyclical deficit at 2.3% of GDP.

£123bill = Structural deficit at

Again this can be split into £73bill current and £50bill investment.

Now the issue in all these numbers relates to what would be needed to get the economy back on a sound footing in the medium term, say 2014/15. How strong would be the cyclical bounceback and when would it start? All the info available seemed to show that it had started and that it would be larger than the Treasury’s “conservative” forecasts seemed to suggest.

The numbers above are the OBR view after they moved £12bill from the cyclical deficit to the structural deficit. All on the back of a dodgy Treasury view which they then made more extreme with some judiciously timed changes to the trend growth rate.

It is at this point that all those of a conspiratorial nature should look away just in case they would want to impugn the pristine reputation of the “Three Brothers Grimm” or Sniffy’s Beard as they are colloquially known in the environs of G1.

Now take the OBR changes out of the equation and the current part of the structural deficit then reduces to £61bill, or a lot less threatening than the £156bill headline figure, remembering that even this figure is based on the Treasury output gap of 6% which seems low given the scale of the Credit Crunch Recession and the state of the country at the moment.

It is in this context that AD’s £18bill of tax rises and £39bill of cuts needs to be seen.

What was being proposed was more than enough to stabilise the economy, the first two months of 2010/11 suggest that the recovery in tax revenues will confound the OBR / Treasury analyses. Finally the output gap and the related cyclical deficit need work so that the current results can be updated to better represent the actual economic conditions of the Credit Crunch.

Credit Crunch = 11% of trend GDP lost

Treasury / Budget View = 6% output gap.

OBR view = 4% output gap

Does the economy you experience appear 4% idle?

Does the economy you experience appear 8% idle?

If the true output gap is 8% does that mean the cyclical deficit is 4.6% of GDP?

If the cyclical gap is 4.6% of GDP does that mean the total structural deficit is £90bill?

If the total structural deficit is £90bill does that mean the current figure is £40bill?

If the current deficit figure is £40bill does that make AD’s £57bill squeeze look prudent?

Finally Sniffy got it wrong by saying that GB/AD didn’t know where the money was going to come from, it is coming from the same place as his £85/90bill slash-fest is coming from. Just a case that AD was not going to get involved with corporate welfare and the patient would have survived the operation.

AD had a plan.

It was a timid Edinburgh lawyer’s plan but it would have worked.

mike

Hughes in his local paper Southwark News was defending Coalition and Budget

he really has been caught out

I think most Lib Dem MPs have been shocked at how the budget has impacted on the poor

……..and they look to the Lib Dem Front bench and then at the Tory front bench and there was no difference

two legs good four legs bad

Jacquie Martin

Simon Hughes is lining up to lead the ??? when they split from the LibDem party. Clegg will join the Tories – the loyal servant he is.

vi__sa, I agree only with the fact that most people would support a higher tax rate. I’d have done it yonks ago. But the recession did account for less tax take. Before then tax and spending ran closely parallel. If spending the taxpayer’s money on keeping the country solvent, then like most businesses, loans are the short term alternative.

Until we have the tax talk, we’ll never fully deal with the deficit. Guess who’ll the ConDems will line up to take the tax hit.